Efficient Frontier with Google Sheets#

![]()

![]()

Description: Efficient Frontier example using Google Sheets

Tags: amplpy, google-sheets, finance

Notebook author: Christian Valente <ccv@ampl.com>

Model author: Harry Markowitz

References:

Markowitz, H.M. (March 1952). “Portfolio Selection”. The Journal of Finance. 7 (1): 77–91. doi:10.2307/2975974. JSTOR 2975974.

Install needed modules and authenticate user to use google sheets#

from google.colab import auth

auth.authenticate_user()

# Install dependencies

%pip install -q amplpy pandas gspread matplotlib

# Google Colab & Kaggle integration

from amplpy import AMPL, ampl_notebook

ampl = ampl_notebook(

modules=["cplex"], # modules to install

license_uuid="default", # license to use

) # instantiate AMPL object and register magics

Auxiliar functions#

import gspread

from google.auth import default

creds, _ = default()

gclient = gspread.authorize(creds)

def open_spreedsheet(name):

if name.startswith("https://"):

return gclient.open_by_url(name)

return gclient.open(name)

import pandas as pd

def get_worksheet_values(name):

return spreedsheet.worksheet(name).get_values(

value_render_option="UNFORMATTED_VALUE"

)

def table_to_dataframe(rows):

return pd.DataFrame(rows[1:], columns=rows[0]).set_index(rows[0][0])

def matrix_to_dataframe(rows, tr=False, nameOverride=None):

col_labels = rows[0][1:]

row_labels = [row[0] for row in rows[1:]]

def label(pair):

return pair if not tr else (pair[1], pair[0])

data = {

label((rlabel, clabel)): rows[i + 1][j + 1]

for i, rlabel in enumerate(row_labels)

for j, clabel in enumerate(col_labels)

}

df = pd.Series(data).reset_index()

name = nameOverride if nameOverride else rows[0][0]

df.columns = ["index1", "index2", name]

return df.set_index(["index1", "index2"])

Efficient Frontier Example#

Open connection to the spreadsheet and get the data, using the utility functions in ampltools to get pandas dataframes.

spreedsheet = open_spreedsheet(

"https://docs.google.com/spreadsheets/d/1d9wRk2PJgYsjiNVoKi1FcawGSVUB5mxSeQUBdEleUv4/edit?usp=sharing"

)

rows = get_worksheet_values("covariance")

# To be able to use ampl.set_data, we override the data column

# of the dataframe to the name of the parameter we will be setting (S)

covar = matrix_to_dataframe(rows, nameOverride="S")

rows = get_worksheet_values("expectedReturns")

expected = table_to_dataframe(rows)

The following is a version of Markowitz mean-variance model, that can be used to calculate the efficient frontier

%%ampl_eval

set A ordered; # assets

param S{A, A}; # cov matrix

param mu{A} default 0; # expected returns

param lb default 0;

param ub default Infinity;

param targetReturn default -Infinity;

var w{A} >= lb <= ub; # weights

var portfolioReturn >= targetReturn;

minimize portfolio_variance: sum {i in A, j in A} S[i, j] * w[i] * w[j];

maximize portfolio_return: sum{a in A} mu[a] * w[a];

s.t. def_total_weight: sum {i in A} w[i] = 1;

s.t. def_target_return: sum{a in A} mu[a] * w[a] >= targetReturn;

Using amplpy we set the data of the ampl entities using the dataframes we got from google sheets

# Set expected returns

ampl.set_data(expected, set_name="A")

# Set covariance data

ampl.set_data(covar)

Set a few options in AMPL to streamline the execution

%%ampl_eval

# Set options

option solver cplex;

option solver_msg 0;

# The following declarations are needed for the efficient frontier script

param nPoints := 20;

param minReturn;

param maxReturn;

param variances{1..nPoints+1};

param returns{1..nPoints+1};

param delta = (maxReturn-minReturn)/nPoints;

Calculate the extreme points for the efficient frontier procedure: get the minimum return by solving the min varance problem, then get the maximum return by solving the max return problem.

%%ampl_eval

# Solve the min variance problem to get the minimum return

objective portfolio_variance;

solve > NUL;

printf "Min portfolio variance: %f, return: %f\n", portfolio_variance, portfolio_return;

let minReturn := portfolio_return;

# Store the first data point in the efficient frontier

let variances[1] := portfolio_variance;

let returns[1] := minReturn;

# Solve the max return problem

objective portfolio_return;

solve > NUL;

printf "Max portfolio variance: %f, return: %f", portfolio_variance, portfolio_return;

let maxReturn := portfolio_return;

Min portfolio variance: 0.000092, return: 0.001530

Max portfolio variance: 0.000249, return: 0.002182

Now that we have the upper and lower values for the expected returns, iterate nPoints times setting the desired return at regularly increasing levels and solve the min variance problem, thus getting the points (return - variance) needed to plot the efficient frontier.

%%ampl_eval

# Switch objective to portfolio variance

objective portfolio_variance;

# Set starting point

let targetReturn := minReturn;

# Calculate the efficient frontier

for{j in 1..nPoints}

{

let targetReturn := targetReturn+delta;

solve > NUL;

printf "Return %f, variance %f\n", portfolio_return, portfolio_variance;

let returns[j+1] := portfolio_return;

let variances[j+1]:=portfolio_variance;

};

Return 0.001563, variance 0.000092

Return 0.001596, variance 0.000092

Return 0.001628, variance 0.000092

Return 0.001661, variance 0.000093

Return 0.001693, variance 0.000093

Return 0.001726, variance 0.000094

Return 0.001758, variance 0.000094

Return 0.001791, variance 0.000095

Return 0.001823, variance 0.000096

Return 0.001856, variance 0.000097

Return 0.001889, variance 0.000099

Return 0.001921, variance 0.000100

Return 0.001954, variance 0.000101

Return 0.001986, variance 0.000104

Return 0.002019, variance 0.000110

Return 0.002051, variance 0.000118

Return 0.002084, variance 0.000129

Return 0.002116, variance 0.000144

Return 0.002149, variance 0.000182

Return 0.002182, variance 0.000249

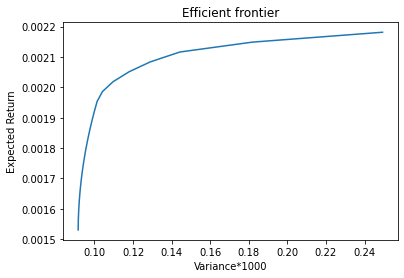

Finally, we plot the efficient frontier

import matplotlib.pyplot as plt

df = ampl.get_data("returns", "variances").to_pandas()

plt.plot(df.variances * 1000, df.returns)

plt.xlabel("Variance*1000")

plt.ylabel("Expected Return")

plt.title("Efficient frontier")

plt.show()