Solving simple stochastic optimization problems with AMPL#

![]()

![]()

![]()

Description: Examples of the Sample Average Approximation method and risk measures in AMPL

Tags: AMPL, amplpy, Stochastic Optimization, Sample Average Approximation, Risk measures

Notebook author: Nicolau Santos <nicolau@ampl.com>

# Install dependencies

%pip install -q amplpy pandas matplotlib numpy

# Google Colab & Kaggle integration

from amplpy import AMPL, ampl_notebook

ampl = ampl_notebook(

modules=["highs"], # modules to install

license_uuid="default", # license to use

) # instantiate AMPL object and register magics

This notebook is based on the Gurobi webinar and materials available at https://www.gurobi.com/events/solving-simple-stochastic-optimization-problems-with-gurobi/ and has examples of the Sample Average Approximation method and risk measures in AMPL. The original version featured the Gurobi solver. By default, this notebook uses the Highs solver, so that all users are able to change and solve the models in the notebook. It’s possible to choose a different solver directly changing the solver variable. Note that the MIP in the examples is hard to solve and open source solvers will strugle to find a good solutions for it.

This notebook features the newsvendor problem. The newsvendor problem has the following characteristics:

You have to buy today a stock of products to sell tomorrow.

The demand is unknown.

It is possible to salvage the remaining stock (sell for scrap).

The presented solutions are:

Manual solution

Maximize expected returns

Maximize worst case

Maximize worst alpha percentile

Minimize Conditionnal Value at Risk (CVaR)

Maximize mixture of CVaR and Expected value

import random

from amplpy import AMPL

import matplotlib.pyplot as plt

from matplotlib import colors

from matplotlib import gridspec

from matplotlib.ticker import PercentFormatter

import numpy

import pandas as pd

random.seed(a=100)

n_bins = 150

dpi = 120

solver = "highs"

# Conditional value at risk (for losses) is the expected value of the worst alpha% tail of the realizations

# in the random variable (represented in this case as a list of values)

# alpha: a value in ]0,1[

# data: a list of values

def CVaR(data, alpha):

data.sort()

n = len(data)

m = int(alpha * n)

return sum(data[m:-1]) / len(data[m:-1])

# Prints the double histogram of a random variable (represented in this case as a list of values)

# First the empirical density distribution, and then the empirical accumulated probability

def doubleHist(data, xlabel=None):

# plt.figure(figsize=(14.5,6),dpi=100)

plt.figure(figsize=(10, 6), dpi=dpi)

gs = gridspec.GridSpec(2, 1, height_ratios=[5, 1], wspace=0.25)

ax = plt.subplot(gs[0])

ax3 = plt.subplot(gs[1])

ax.grid(True)

ax.set_title(xlabel)

ax.set_ylabel("Likelihood of occurrence", color="blue")

ax2 = ax.twinx()

ax2.set_ylabel("Cumulative probability", color="red")

# plot the density and cumulative histogram

n, bins, patches = ax.hist(

data,

n_bins,

density=True,

alpha=0.65,

cumulative=False,

label="Density",

color="blue",

)

n, bins, patches = ax2.hist(

data,

n_bins,

density=True,

histtype="step",

cumulative=True,

label="CDF",

color="red",

)

ax3.boxplot(data, vert=False, whis=[5, 95])

# ax3.axis("off")

ax3.tick_params(

left=False,

right=False,

labelleft=False,

labelbottom=False,

bottom=False,

top=True,

)

# tidy up the figure

plt.show()

# Print basic info on a given solution

def solutionStats(model, losses):

global cost

losses.sort()

samples = len(losses)

order = model.var["order"].value()

print(

"Model Value",

model.get_objective("obj").value(),

"order Qty",

order,

"investment",

order * cost,

"#samples",

samples,

)

print("Losses stats:")

print(

"CVaR(95%,90%,80%,70%)",

CVaR(losses, 0.95),

CVaR(losses, 0.90),

CVaR(losses, 0.80),

CVaR(losses, 0.70),

)

print(

"min",

min(losses),

"max",

max(losses),

"average",

sum(losses) / samples,

"VaR_75%",

losses[int(0.75 * samples)],

)

# Build a dataframe with expected values and CVaR values specified in the cvars list

def getTable(data, colnames, cvars):

info = []

temp = ["Expected Value"]

for sol in data:

temp.append(sum(sol) / len(sol))

info.append(temp)

for c in cvars:

temp = ["CVaR_" + str(c) + "%"]

for sol in data:

temp.append(CVaR(sol, c / 100))

info.append(temp)

return pd.DataFrame(info, columns=["Metric"] + colnames)

# Get the list of losses from the AMPL instance

def getLosses(ampl):

return [-v[1] for v in ampl.var["profit"].getValues()]

# Define constants

# Basic economic parameters

# cost: is the procurement cost of each unit

# retail: selling price

# recover: scrap price (if negative is a cost, MUST be smaller than cost, otherwise problem is unbounded!)

cost = 2

retail = 15

recover = -3

# By sampling, we approximate integrals....

# The larger the sample, the more accurate.... but the harder the problem

samples = 10000

# we have a (positive truncated) normal distribution for demand (can't have a negative demand... unless short selling....)

sigma = 100

mu = 400

demand = [max(random.normalvariate(mu, sigma), 0) for i in range(samples)]

# Maximum and minimum revenue. Will be used to bound variables

maxrev = max(demand) * (retail - cost)

minrev = max(demand) * (recover - cost) + min(demand) * retail

Manual solution#

order = 600

losses = [

-retail * min(order, demand[i]) + cost * order - recover * max(0, order - demand[i])

for i in range(samples)

]

Explore solution#

sol = losses.copy()

sol.sort()

print(

"Solution Value",

-sum(sol) / len(sol),

"order Qty",

order,

"investment",

order * cost,

"#samples",

samples,

)

print("Losses stats:")

print(

"CVaR(95%,90%,80%,70%)",

CVaR(sol, 0.95),

CVaR(sol, 0.90),

CVaR(sol, 0.80),

CVaR(sol, 0.70),

)

print(

"min",

min(sol),

"max",

max(sol),

"average",

sum(sol) / samples,

"VaR_75%",

sol[int(0.75 * samples)],

)

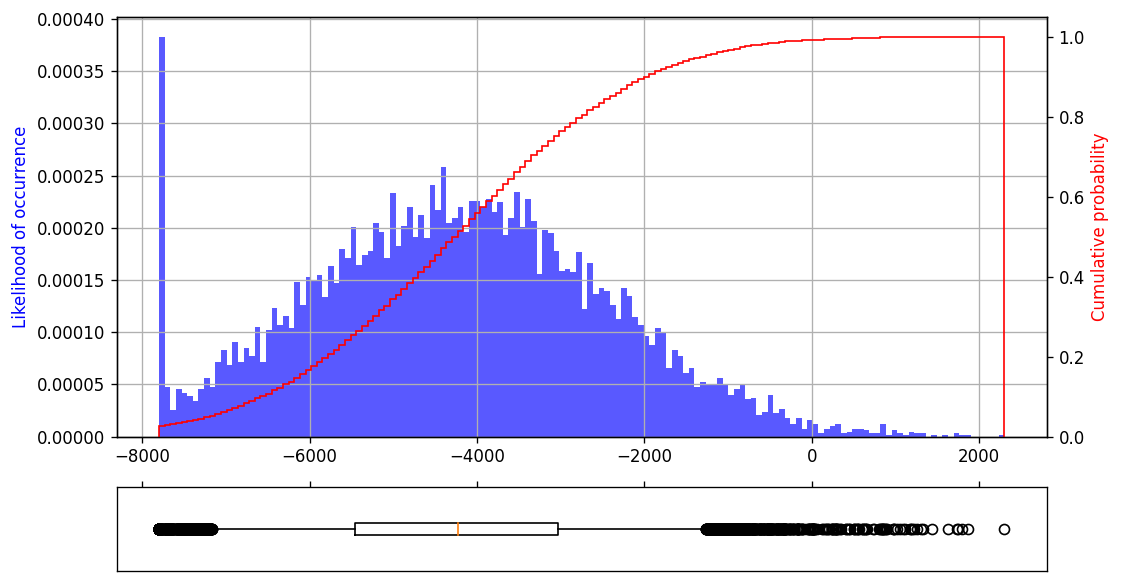

doubleHist(sol)

Solution Value 4218.884025261554 order Qty 600 investment 1200 #samples 10000

Losses stats:

CVaR(95%,90%,80%,70%) -548.3178927360779 -1098.2236361473692 -1725.803157600196 -2157.3548113755487

min -7800 max 2301.589271028297 average -4218.884025261554 VaR_75% -3029.6614816227075

Maximize expected returns#

%%writefile model1.mod

param samples > 0; # number of samples

param demand{1..samples} >= 0; # demand for each sample

param cost > 0; # procurement cost of each unit

param retail >= 0; # selling price of each unit

param recover < cost; # liquidation price of each unit

param minrev; # bound on minimum revenue

param maxrev; # bound on maximum revenue

var order >= 0; # number of units to order

var sales{i in 1..samples} >= 0, <= demand[i]; # sales of each sample

var discount{1..samples} >= 0; # scraped units of each sample

var profit{1..samples} >= minrev, <= maxrev; # profit of each sample

# maximize average profit across all samples

maximize obj: (1/samples) * sum{i in 1..samples} profit[i];

# profit of each sample

s.t. sample_profit {i in 1..samples}: profit[i] == -cost * order + retail * sales[i] + recover * discount[i];

# sales and discount of each sample

s.t. sample_sales {i in 1..samples}: sales[i] + discount[i] == order;

Writing model1.mod

# Create AMPL instance and load the model

ampl = AMPL()

ampl.read("model1.mod")

# Load the data

ampl.param["samples"] = samples

ampl.param["cost"] = cost

ampl.param["recover"] = recover

ampl.param["retail"] = retail

ampl.param["minrev"] = minrev

ampl.param["maxrev"] = maxrev

ampl.param["demand"] = demand

# Set options and solve

ampl.option["highs_options"] = "outlev=1"

ampl.solve(solver=solver)

assert ampl.solve_result == "solved", ampl.solve_result

HiGHS 1.5.1: tech:outlev=1

Running HiGHS 1.5.1 [date: 2023-02-27, git hash: 93f1876]

Copyright (c) 2023 HiGHS under MIT licence terms

Presolving model

20000 rows, 30001 cols, 70000 nonzeros

20000 rows, 30001 cols, 70000 nonzeros

Presolve : Reductions: rows 20000(-0); columns 30001(-0); elements 70000(-0) - Not reduced

Problem not reduced by presolve: solving the LP

Using EKK dual simplex solver - serial

Iteration Objective Infeasibilities num(sum)

0 0.0000000000e+00 Ph1: 0(0) 0s

20000 4.6223579332e+03 Pr: 0(0) 3s

Model status : Optimal

Simplex iterations: 20000

Objective value : 4.6223579332e+03

HiGHS run time : 3.41

HiGHS 1.5.1: optimal solution; objective 4622.357933

20000 simplex iterations

0 barrier iterations

Explore solution#

sol1 = getLosses(ampl)

solutionStats(ampl, sol1)

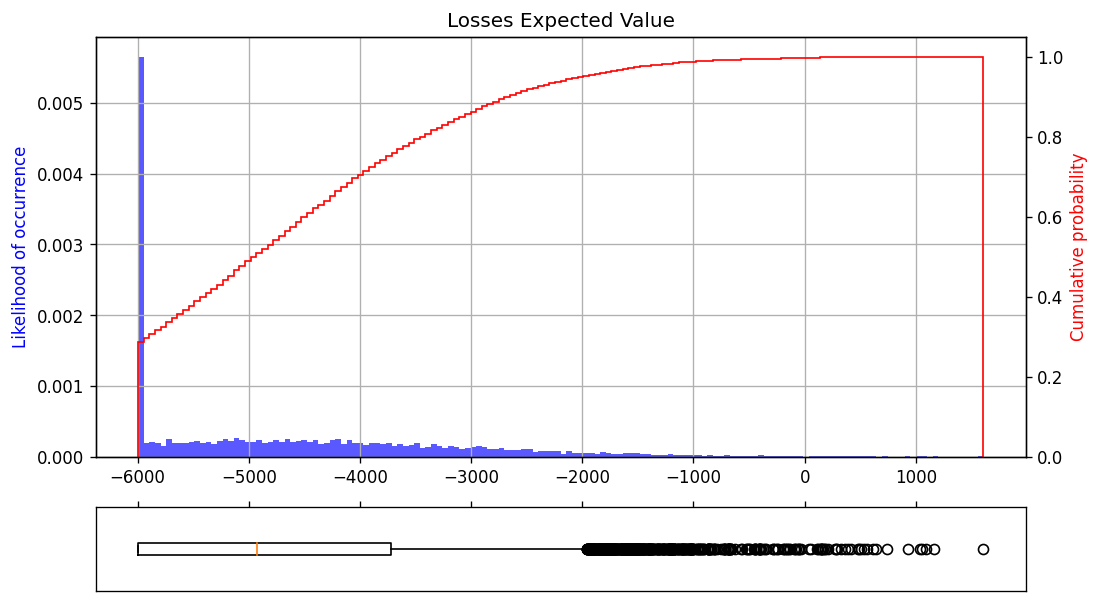

doubleHist(sol1, xlabel="Losses Expected Value")

Model Value 4622.357933244379 order Qty 461.2352777789903 investment 922.4705555579806 #samples 10000

Losses stats:

CVaR(95%,90%,80%,70%) -1242.1415038411253 -1792.0472472524186 -2419.626768705242 -2851.1784224805892

min -5996.058611126874 max 1607.765659923248 average -4622.357933244431 VaR_75% -3723.485092727757

Maximize worst case#

%%writefile model2.mod

param samples > 0; # number of samples

param demand{1..samples} >= 0; # demand for each sample

param cost > 0; # procurement cost of each unit

param retail >= 0; # selling price of each unit

param recover < cost; # liquidation price of each unit

param minrev; # bound on minimum revenue

param maxrev; # bound on maximum revenue

var order >= 0; # number of units to order

var sales{i in 1..samples} >= 0, <= demand[i]; # sales of each sample

var discount{1..samples} >= 0; # scraped units of each sample

var profit{1..samples} >= minrev, <= maxrev; # profit of each sample

var worst >= minrev, <= maxrev; # worst profit

# maximize worst case

maximize obj: worst;

# profit of each sample

s.t. sample_profit {i in 1..samples}: profit[i] == -cost * order + retail * sales[i] + recover * discount[i];

# sales and discount of each sample

s.t. sample_sales {i in 1..samples}: sales[i] + discount[i] == order;

# bound worst across all samples

s.t. worst_case {i in 1..samples}: worst <= profit[i];

Writing model2.mod

# Create AMPL instance and load the model

ampl = AMPL()

ampl.read("model2.mod")

# Load the data

ampl.param["samples"] = samples

ampl.param["cost"] = cost

ampl.param["recover"] = recover

ampl.param["retail"] = retail

ampl.param["minrev"] = minrev

ampl.param["maxrev"] = maxrev

ampl.param["demand"] = demand

# Set options and solve

ampl.option["highs_options"] = "outlev=1"

ampl.solve(solver=solver)

assert ampl.solve_result == "solved", ampl.solve_result

HiGHS 1.5.1: tech:outlev=1

Running HiGHS 1.5.1 [date: 2023-02-27, git hash: 93f1876]

Copyright (c) 2023 HiGHS under MIT licence terms

Presolving model

30000 rows, 30002 cols, 90000 nonzeros

20040 rows, 20042 cols, 70080 nonzeros

20040 rows, 20042 cols, 70080 nonzeros

Presolve : Reductions: rows 20040(-9960); columns 20042(-9960); elements 70080(-19920)

Solving the presolved LP

Using EKK dual simplex solver - serial

Iteration Objective Infeasibilities num(sum)

0 0.0000000000e+00 Ph1: 0(0) 0s

10041 -5.0440774870e+02 Pr: 0(0) 1s

Solving the original LP from the solution after postsolve

Model status : Optimal

Simplex iterations: 10041

Objective value : 5.0440774870e+02

HiGHS run time : 1.13

HiGHS 1.5.1: optimal solution; objective 504.4077487

10041 simplex iterations

0 barrier iterations

Explore solution#

sol2 = getLosses(ampl)

solutionStats(ampl, sol2)

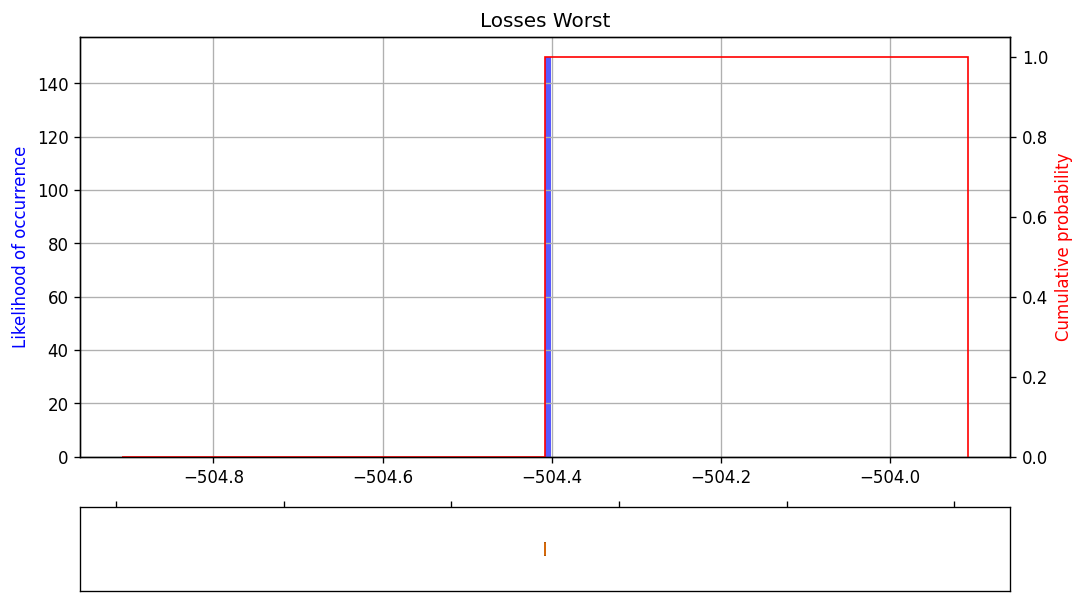

doubleHist(sol2, xlabel="Losses Worst")

Model Value 504.4077487017854 order Qty 38.8005960539835 investment 77.601192107967 #samples 10000

Losses stats:

CVaR(95%,90%,80%,70%) -504.40774870178035 -504.40774870179337 -504.40774870177256 -504.40774870176483

min -504.4077487017854 max -504.4077487017854 average -504.40774870189 VaR_75% -504.4077487017854

Maximize worst alpha percentile (\(\alpha\)-Value at Risk)#

%%writefile model3.mod

param samples > 0; # number of samples

param demand{1..samples} >= 0; # demand for each sample

param cost > 0; # procurement cost of each unit

param retail >= 0; # selling price of each unit

param recover < cost; # liquidation price of each unit

param minrev; # bound on minimum revenue

param maxrev; # bound on maximum revenue

param alpha >= 0, <= 1; # value at risk

var order >= 0; # number of units to order

var sales{i in 1..samples} >= 0, <= demand[i]; # sales of each sample

var discount{1..samples} >= 0; # scraped units of each sample

var profit{1..samples} >= minrev, <= maxrev; # profit of each sample

var worst >= minrev, <= maxrev; # worst profit

var chance{1..samples} binary; # chance of each sample

# maximize worst alpha percentile

maximize obj: worst;

# profit of each sample

s.t. sample_profit {i in 1..samples}: profit[i] == -cost * order + retail * sales[i] + recover * discount[i];

# sales and discount of each sample

s.t. sample_sales {i in 1..samples}: sales[i] + discount[i] == order;

# relation between worst, chance and profit

s.t. sample_chance {i in 1..samples}: worst - (maxrev - minrev) * chance[i] <= profit[i];

# percentile

s.t. c4: sum{i in 1..samples} chance[i] <= samples * (1 - alpha);

Writing model3.mod

alpha = 0.75

# Create AMPL instance and load the model

ampl = AMPL()

ampl.read("model3.mod")

# Load the data

ampl.param["samples"] = samples

ampl.param["cost"] = cost

ampl.param["recover"] = recover

ampl.param["retail"] = retail

ampl.param["minrev"] = minrev

ampl.param["maxrev"] = maxrev

ampl.param["demand"] = demand

ampl.param["alpha"] = alpha

# Set options and solve

ampl.option["highs_options"] = "outlev=1 timelim=60.0"

ampl.solve(solver=solver)

assert ampl.solve_result in ["solved", "limit"], ampl.solve_result

HiGHS 1.5.1: tech:outlev=1

lim:time=60

Running HiGHS 1.5.1 [date: 2023-02-27, git hash: 93f1876]

Copyright (c) 2023 HiGHS under MIT licence terms

Presolving model

30001 rows, 40002 cols, 110000 nonzeros

30001 rows, 40002 cols, 100000 nonzeros

Solving MIP model with:

30001 rows

40002 cols (10000 binary, 0 integer, 0 implied int., 30002 continuous)

100000 nonzeros

Nodes | B&B Tree | Objective Bounds | Dynamic Constraints | Work

Proc. InQueue | Leaves Expl. | BestBound BestSol Gap | Cuts InLp Confl. | LpIters Time

0 0 0 0.00% 10067.433634 -inf inf 0 0 0 0 13.4s

R 0 0 0 0.00% 10067.433634 874.5936399 1051.10% 0 0 0 36169 61.0s

Solving report

Status Time limit reached

Primal bound 874.593639936

Dual bound 10067.4336338

Gap 1051.1% (tolerance: 0.01%)

Solution status feasible

874.593639936 (objective)

0 (bound viol.)

0 (int. viol.)

0 (row viol.)

Timing 61.06 (total)

13.31 (presolve)

0.00 (postsolve)

Nodes 0

LP iterations 36169 (total)

0 (strong br.)

0 (separation)

0 (heuristics)

HiGHS 1.5.1: interrupted

36169 simplex iterations

0 branching nodes

absmipgap=9192.84, relmipgap=10.511

Explore solution#

sol3 = getLosses(ampl)

solutionStats(ampl, sol3)

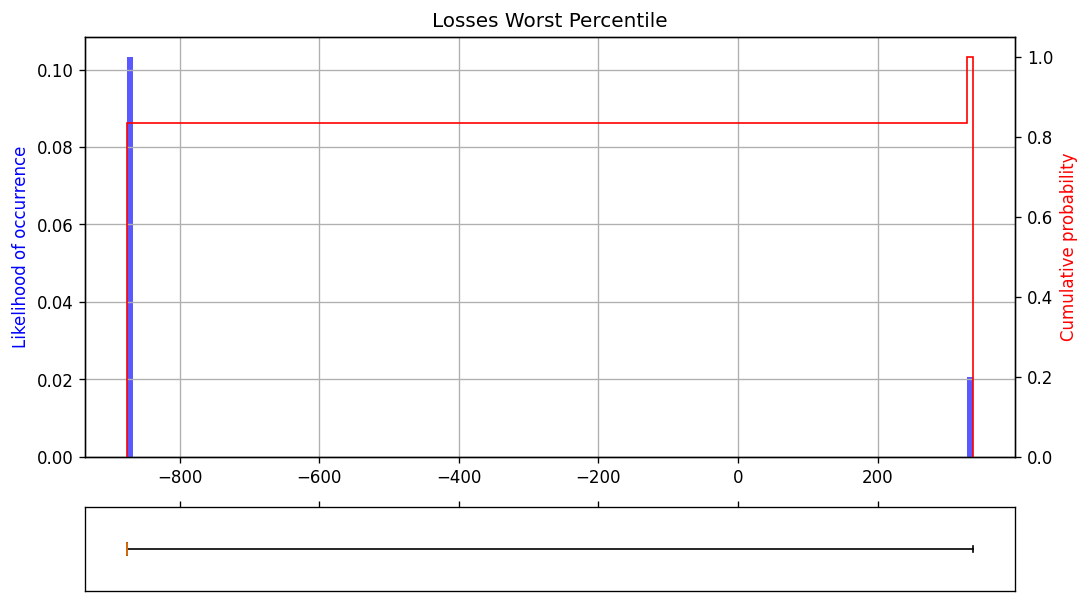

doubleHist(sol3, xlabel="Losses Worst Percentile")

Model Value 874.593639936231 order Qty 67.27643384124855 investment 134.5528676824971 #samples 10000

Losses stats:

CVaR(95%,90%,80%,70%) 336.3821692062457 336.38216920624063 126.77855241620063 -207.12347904508792

min -874.593639936231 max 336.3821692062427 average -674.2982411040476 VaR_75% -874.593639936231

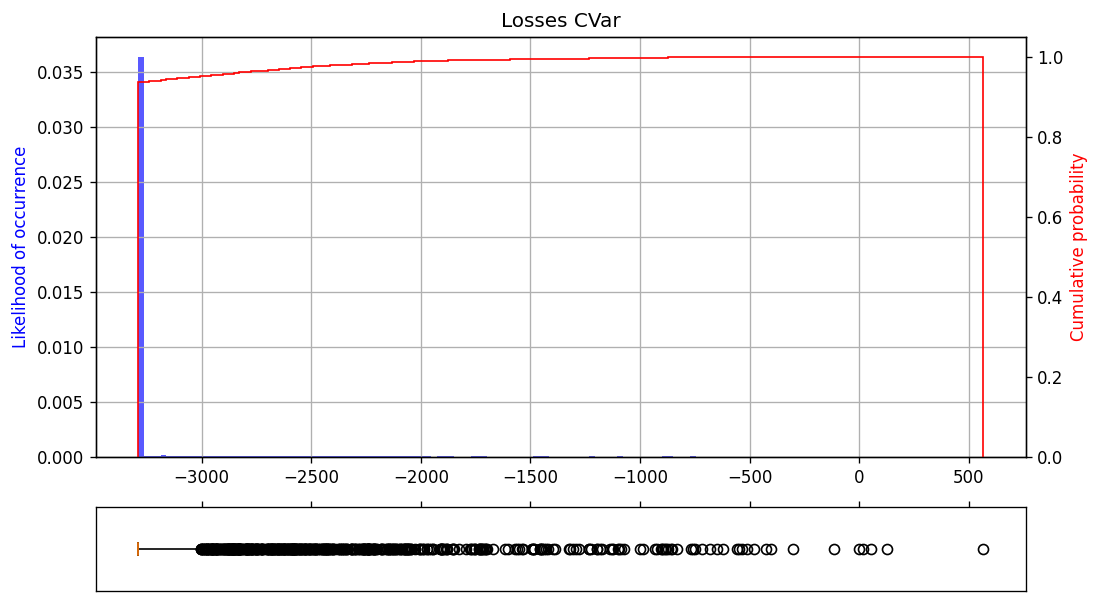

Minimize Conditional Value at Risk (\(CVaR_\alpha\))#

%%writefile model4.mod

param samples > 0; # number of samples

param demand{1..samples} >= 0; # demand for each sample

param cost > 0; # procurement cost of each unit

param retail >= 0; # selling price of each unit

param recover < cost; # liquidation price of each unit

param minrev; # bound on minimum revenue

param maxrev; # bound on maximum revenue

param alpha >= 0, <= 1; # value at risk

var order >= 0; # number of units to order

var sales{i in 1..samples} >= 0, <= demand[i]; # sales of each sample

var discount{1..samples} >= 0; # scraped units of each sample

var profit{1..samples} >= minrev, <= maxrev; # profit of each sample

var nu >= minrev, <= maxrev;

var excess{1..samples} >= 0, <= maxrev - minrev;

# minimize CVaR

minimize obj: nu + (1.0 / ((1 - alpha) * samples)) * sum{i in 1..samples} excess[i];

# profit of each sample

s.t. sample_profit {i in 1..samples}: profit[i] == -cost * order + retail * sales[i] + recover * discount[i];

# sales and discount of each sample

s.t. sample_sales {i in 1..samples}: sales[i] + discount[i] == order;

# relation between excess and profit of each sample

s.t. sample_excess {i in 1..samples}: -profit[i] - nu <= excess[i];

Writing model4.mod

alpha = 0.75

# Create AMPL instance and load the model

ampl = AMPL()

ampl.read("model4.mod")

# Load the data

ampl.param["samples"] = samples

ampl.param["cost"] = cost

ampl.param["recover"] = recover

ampl.param["retail"] = retail

ampl.param["minrev"] = minrev

ampl.param["maxrev"] = maxrev

ampl.param["demand"] = demand

ampl.param["alpha"] = alpha

# Set options and solve

ampl.option["highs_options"] = "outlev=1"

ampl.solve(solver=solver)

assert ampl.solve_result == "solved", ampl.solve_result

HiGHS 1.5.1: tech:outlev=1

Running HiGHS 1.5.1 [date: 2023-02-27, git hash: 93f1876]

Copyright (c) 2023 HiGHS under MIT licence terms

Presolving model

30000 rows, 40002 cols, 100000 nonzeros

30000 rows, 40002 cols, 100000 nonzeros

Presolve : Reductions: rows 30000(-0); columns 40002(-0); elements 100000(-0) - Not reduced

Problem not reduced by presolve: solving the LP

Using EKK dual simplex solver - serial

Iteration Objective Infeasibilities num(sum)

0 -3.3023918373e+03 Pr: 20000(5.14075e+06) 0s

9330 -3.2924042645e+03 Pr: 11868(1.37834e+06) 5s

28358 -3.0786916352e+03 Pr: 0(0); Du: 2(0.322954) 10s

30651 -3.0786916352e+03 Pr: 0(0) 13s

30651 -3.0786916352e+03 Pr: 0(0) 13s

Model status : Optimal

Simplex iterations: 30651

Objective value : -3.0786916352e+03

HiGHS run time : 13.56

HiGHS 1.5.1: optimal solution; objective -3078.691635

30651 simplex iterations

0 barrier iterations

Explore solution#

sol4 = getLosses(ampl)

solutionStats(ampl, sol4)

doubleHist(sol4, xlabel="Losses CVar")

Model Value -3078.691635183291 order Qty 253.0831475661703 investment 506.1662951323406 #samples 10000

Losses stats:

CVaR(95%,90%,80%,70%) -2282.902154905224 -2764.9396550818556 -3027.641637712309 -3115.1505675716676

min -3290.080918360214 max 567.0050088591486 average -3237.233597566205 VaR_75% -3290.080918360214

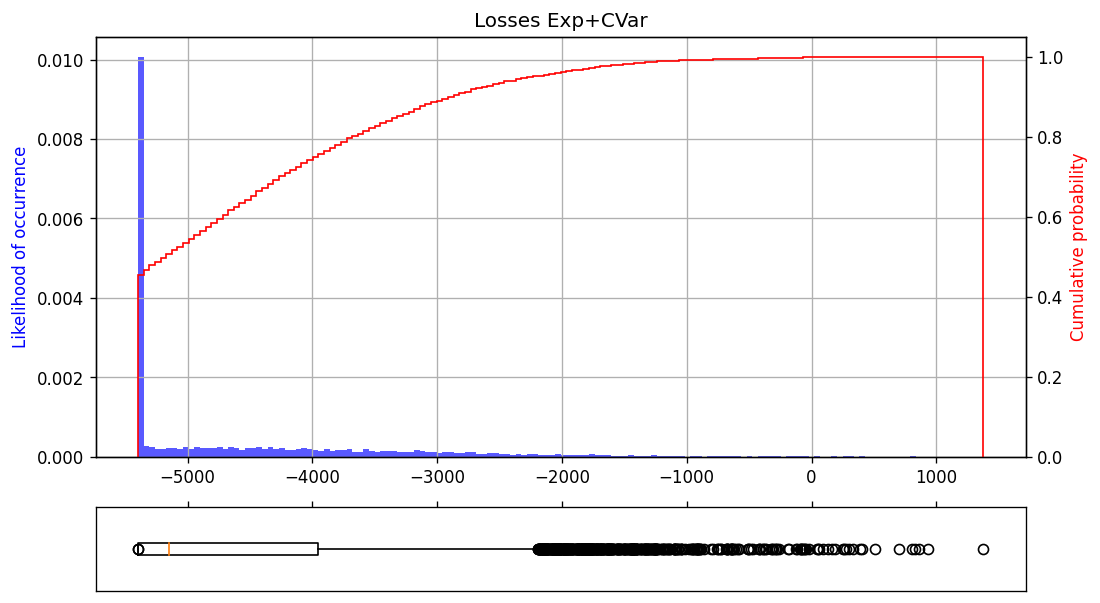

Mixture of CVaR and Expected value#

%%writefile model5.mod

param samples > 0; # number of samples

param demand{1..samples} >= 0; # demand for each sample

param cost > 0; # procurement cost of each unit

param retail >= 0; # selling price of each unit

param recover < cost; # liquidation price of each unit

param minrev; # bound on minimum revenue

param maxrev; # bound on maximum revenue

param alpha >= 0, <= 1; # value at risk

param beta >= 0, <= 1; # weight between expected value and CVaR

var order >= 0; # number of units to order

var sales{i in 1..samples} >= 0, <= demand[i]; # sales of each sample

var discount{1..samples} >= 0; # scraped units of each sample

var profit{1..samples} >= minrev, <= maxrev; # profit of each sample

var nu >= minrev, <= maxrev;

var excess{1..samples} >= 0, <= maxrev - minrev;

# maximize weighted sum of expected value and CVaR

maximize obj:

- beta * nu

- (beta / ((1 - alpha) * samples)) * sum{i in 1..samples} excess[i]

+ ((1-beta)/samples) * sum{i in 1..samples} profit[i];

# profit of each sample

s.t. sample_profit {i in 1..samples}: profit[i] == -cost * order + retail * sales[i] + recover * discount[i];

# sales and discount of each sample

s.t. sample_sales {i in 1..samples}: sales[i] + discount[i] == order;

# relation between excess and profit of each sample

s.t. sample_excess {i in 1..samples}: -profit[i] - nu <= excess[i];

Writing model5.mod

beta = 0.50

alpha = 0.75

# Create AMPL instance and load the model

ampl = AMPL()

ampl.read("model5.mod")

# Load the data

ampl.param["samples"] = samples

ampl.param["cost"] = cost

ampl.param["recover"] = recover

ampl.param["retail"] = retail

ampl.param["minrev"] = minrev

ampl.param["maxrev"] = maxrev

ampl.param["demand"] = demand

ampl.param["alpha"] = alpha

ampl.param["beta"] = beta

# Set options and solve

ampl.option["highs_options"] = "outlev=1"

ampl.solve(solver=solver)

assert ampl.solve_result == "solved", ampl.solve_result

HiGHS 1.5.1: tech:outlev=1

Running HiGHS 1.5.1 [date: 2023-02-27, git hash: 93f1876]

Copyright (c) 2023 HiGHS under MIT licence terms

Presolving model

30000 rows, 40002 cols, 100000 nonzeros

30000 rows, 40002 cols, 100000 nonzeros

Presolve : Reductions: rows 30000(-0); columns 40002(-0); elements 100000(-0) - Not reduced

Problem not reduced by presolve: solving the LP

Using EKK dual simplex solver - serial

Iteration Objective Infeasibilities num(sum)

0 0.0000000000e+00 Ph1: 0(0) 0s

18511 3.7045413447e+03 Pr: 5442(14570.3) 5s

21520 3.6476039870e+03 Pr: 0(0) 7s

21520 3.6476039870e+03 Pr: 0(0) 7s

Model status : Optimal

Simplex iterations: 21520

Objective value : 3.6476039870e+03

HiGHS run time : 7.46

HiGHS 1.5.1: optimal solution; objective 3647.603987

21520 simplex iterations

0 barrier iterations

Explore solution#

sol5 = getLosses(ampl)

solutionStats(ampl, sol5)

doubleHist(sol5, xlabel="Losses Exp+CVar")

Model Value 3647.6039869767988 order Qty 415.1543649507064 investment 830.3087299014128 #samples 10000

Losses stats:

CVaR(95%,90%,80%,70%) -1472.5460679825462 -2022.4518113938377 -2650.031332846664 -3081.582986622015

min -5397.006744359185 max 1377.361095781829 average -4554.551834745325 VaR_75% -3953.889656869175

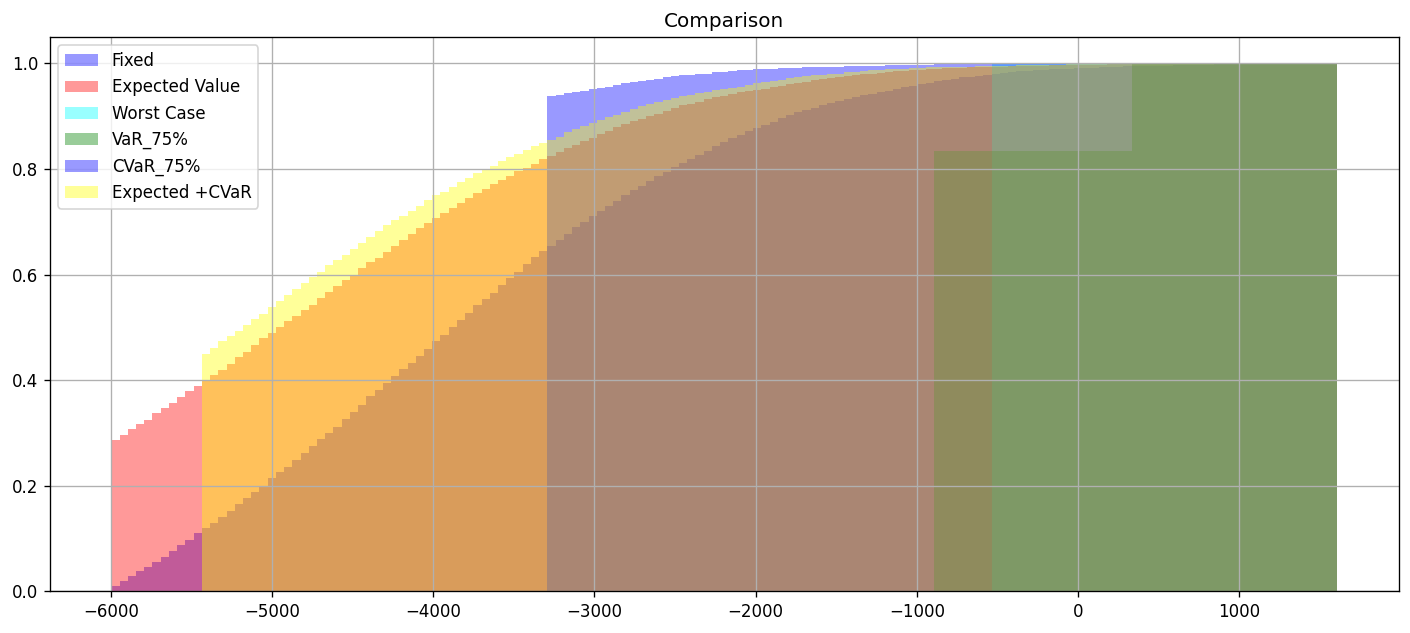

Comparing solution approaches and behavior#

fig, ax = plt.subplots(figsize=(14.5, 6), dpi=dpi)

xmin = min(sol1 + sol2 + sol3 + sol4 + sol5)

xmax = max(sol1 + sol2 + sol3 + sol4 + sol5)

bins = numpy.linspace(xmin, xmax, 150)

ax.grid(True)

ax.set_title("Comparison")

d = True

c = True

a = 0.4

# plot the density and cumulative histogram

n, bins2, patches = ax.hist(

sol, bins, alpha=a, density=d, cumulative=c, label="Fixed", color="blue"

)

n, bins2, patches = ax.hist(

sol1, bins, alpha=a, density=d, cumulative=c, label="Expected Value", color="red"

)

n, bins2, patches = ax.hist(

sol2, bins, alpha=a, density=d, cumulative=c, label="Worst Case", color="cyan"

)

n, bins2, patches = ax.hist(

sol3, bins, alpha=a, density=d, cumulative=c, label="VaR_75%", color="green"

)

n, bins2, patches = ax.hist(

sol4, bins, alpha=a, density=d, cumulative=c, label="CVaR_75%", color="blue"

)

n, bins2, patches = ax.hist(

sol5, bins, alpha=a, density=d, cumulative=c, label="Expected +CVaR", color="yellow"

)

# tidy up the figure

ax.legend(loc="upper left")

plt.show()

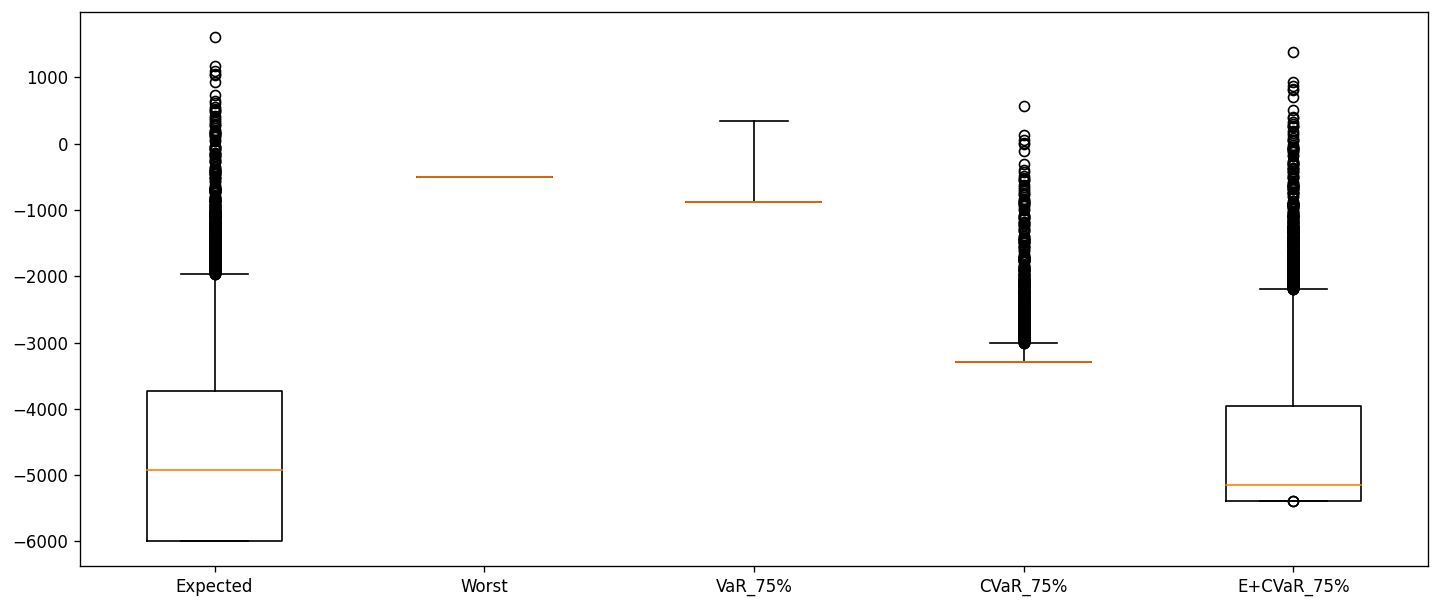

data = [sol1, sol2, sol3, sol4, sol5]

plt.figure(figsize=(14.5, 6), dpi=dpi)

plt.boxplot(data, whis=[5, 95])

plt.xticks([1, 2, 3, 4, 5], ["Expected", "Worst", "VaR_75%", "CVaR_75%", "E+CVaR_75%"])

plt.show()

data = [sol1, sol2, sol3, sol4, sol5]

colnames = ["Expected", "Worst", "VaR_75%", "CVaR_75%", "Ex+CVaR_75%"]

cvars = [70, 80, 90, 95]

display(getTable(data, colnames, cvars))

| Metric | Expected | Worst | VaR_75% | CVaR_75% | Ex+CVaR_75% | |

|---|---|---|---|---|---|---|

| 0 | Expected Value | -4622.357933 | -504.407749 | -674.298241 | -3237.233598 | -4554.551835 |

| 1 | CVaR_70% | -2851.178422 | -504.407749 | -207.123479 | -3115.150568 | -3081.582987 |

| 2 | CVaR_80% | -2419.626769 | -504.407749 | 126.778552 | -3027.641638 | -2650.031333 |

| 3 | CVaR_90% | -1792.047247 | -504.407749 | 336.382169 | -2764.939655 | -2022.451811 |

| 4 | CVaR_95% | -1242.141504 | -504.407749 | 336.382169 | -2282.902155 | -1472.546068 |