Pricing Optimization (Price Elasticity of Demand)#

![]()

![]()

![]()

This model finds the point that maximizes profit based on price elasticity and cost.

Tags: amplpy, MIP, pricing-optimization, demand-elasticity, profit-maximization, economic-modeling, piecewise-linear, cplex

Notebook author: Mikhail Riabtsev <mail@solverytic.com>

1. Model Description#

This notebook describes 3 piecewise linear approaches to dealing with nonlinear dependencies and designed to optimize profit through optimal point or price-step selection based on demand and price parameters. Each approach employs unique strategies to achieve its objectives while adhering to specific constraints.

Key Components#

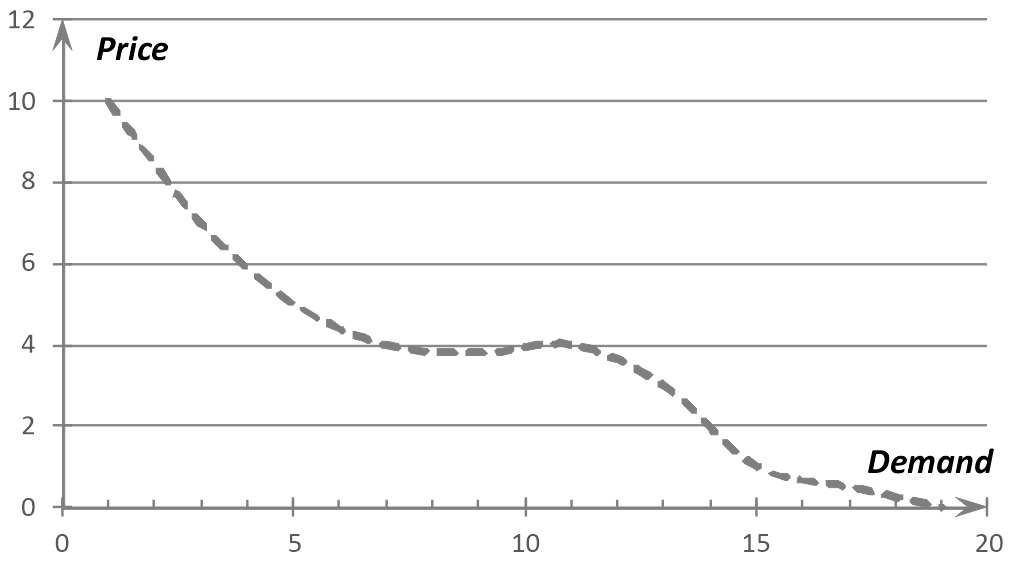

Price-Demand Elastisity Function#

General Parameters#

Demand and Price: Represent demand and price at each point or step, respectively.

Cost: Unit cost (2 $ per unit).

Objective:#

It is necessary to determine the optimal level of sales price in order to obtain maximum profit:

\(\text{Maximize TotalProfit } = \sum_{𝑝 \in POINTS}(price[𝑝] − cost[p]) × demand[𝑝])\)

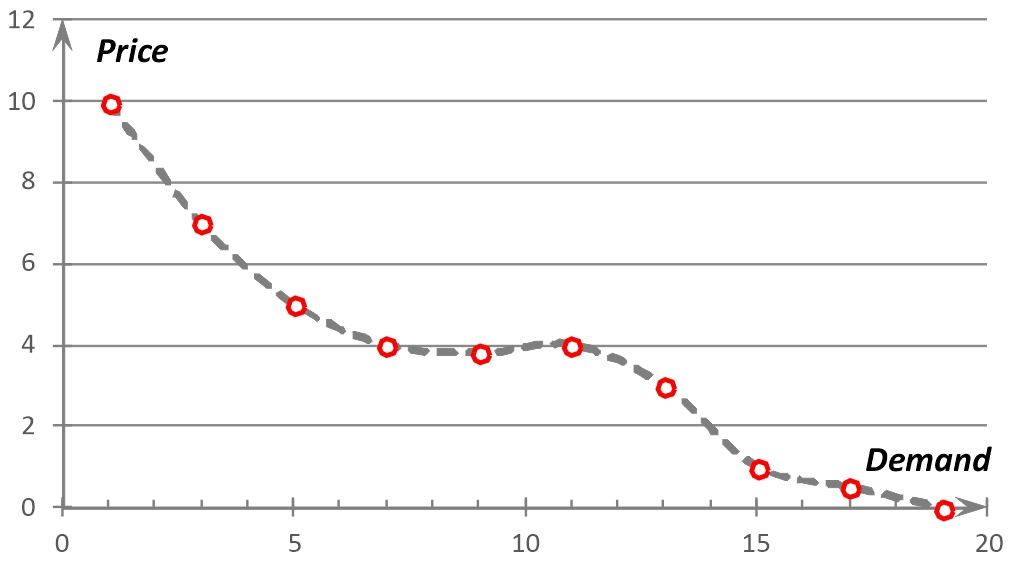

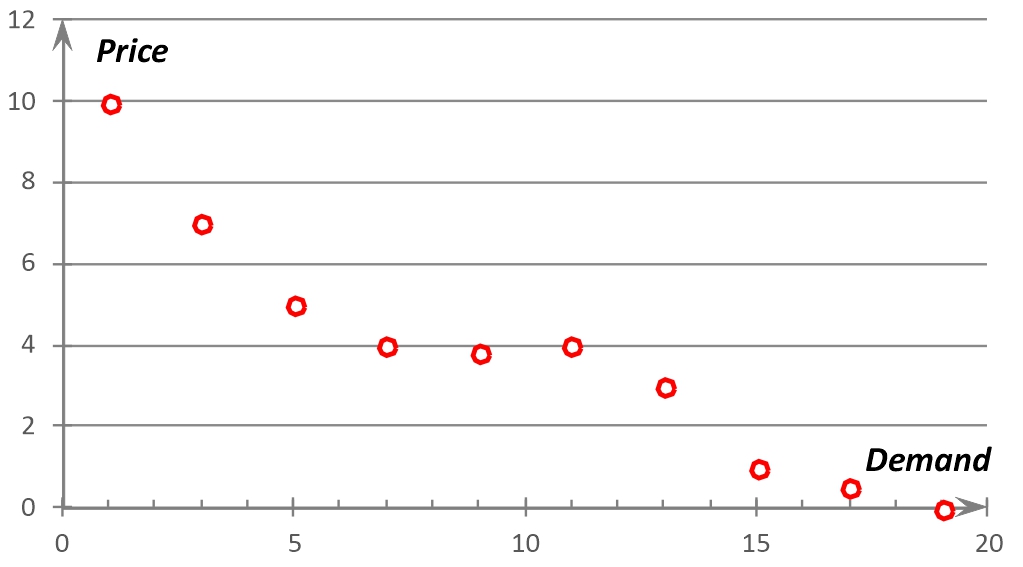

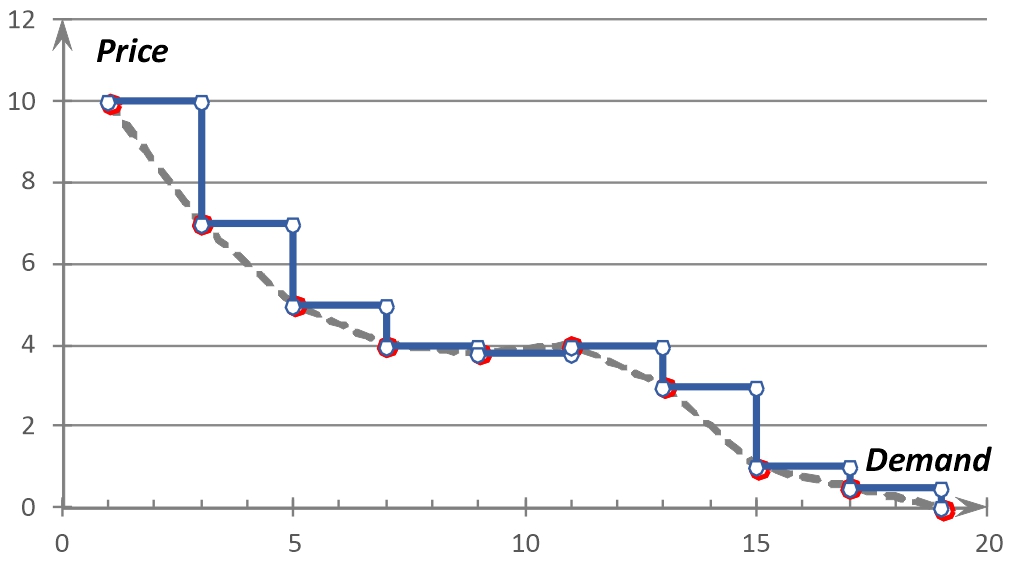

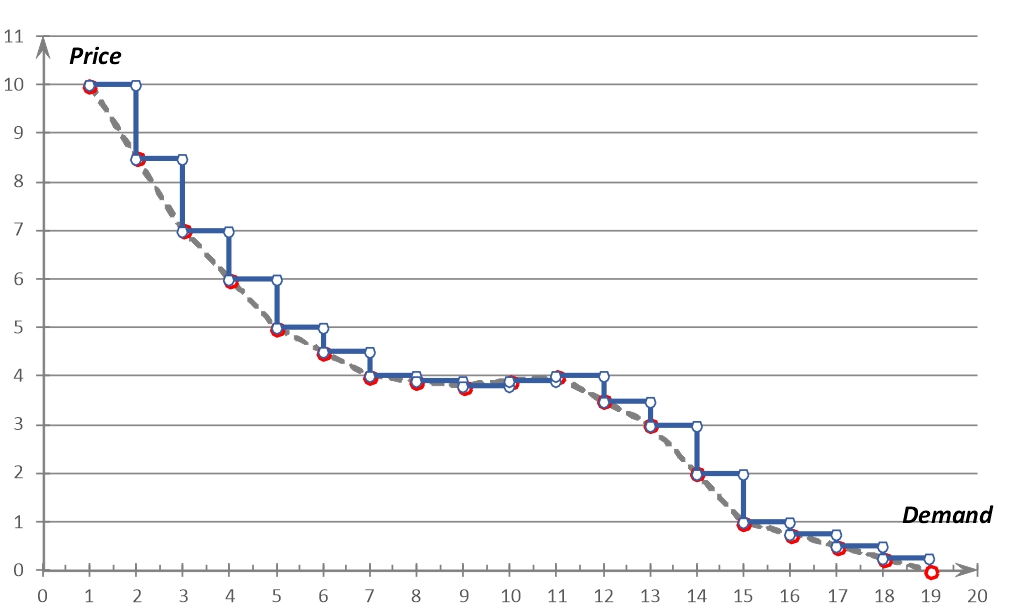

To linearize the existing elasticity of demand function from price changes, we need to select nodal points. The number of selected points and their location on the curve can be any. For the purposes of our project, we will use the following corner points: \([(1, 10), (3, 7), (5, 5), (7, 4), (9, 3.8), (11, 4), (13, 3), (15, 1), (17, 0.5), (19, 0)]\)

2. Download Necessary Extensions and Libraries#

# Install dependencies

%pip install -q amplpy pandas numpy matplotlib scipy

import pandas as pd # Loading panda to work with pandas.DataFrame objects (https://pandas.pydata.org/)

import numpy as np # Loading numpy to perform multidimensional calculations numpy.matrix (https://numpy.org/)

# Google Colab & Kaggle integration

from amplpy import AMPL, ampl_notebook

ampl = ampl_notebook(

modules=["cbc", "highs", "gurobi", "cplex"], # modules to install

license_uuid="default", # license to use

) # instantiate AMPL object and register magics

from amplpy import AMPL

ampl = AMPL() # create a new AMPL object with all default settings

3. Approach#1 (Optimal nodal point)#

This approach determines the nodal point with maximum profit.

3.1. AMPL Model Formulation#

%%writefile demand_elasticity__model.mod

reset;

# Model Name: Pricing Optimization (Price Elasticity of Demand)

# Purpose: Select one point from a set of price level and demand to maximize total profit

# Version: 1.0

# Last Updated: Jan 2025

### SETS & PARAMETERS

# Input parameters defining total quantity, cost, price steps, and demand

param unit_cost >= 0; # Unit cost of the product

param n_step integer > 0; # Number of steps in the piecewise linear price function

param demand {1..n_step} >= 0; # Demand values at each price step

param price {1..n_step} >= 0; # Price values for each demand step

### VARIABLES

# Define decision variables for point selection

var IsSelect {1..n_step} binary; # Binary decision variable: 1 if point is selected, 0 otherwise

### OBJECTIVE

# Maximize total profit based on selected point

maximize TotalProfit:

sum {p in 1..n_step} demand[p] * (price[p] - unit_cost) * IsSelect[p];

### CONSTRAINTS

# Ensure exactly one point is selected

subject to OnePriceSelected:

sum {p in 1..n_step} IsSelect[p] = 1; # Exactly one point is selected

Overwriting demand_elasticity__model.mod

3.2. Load data#

from scipy.interpolate import interp1d

ampl.read("demand_elasticity__model.mod") # Load the AMPL model from the file

# Data for demand and price

data = [

(1, 10),

(3, 7),

(5, 5),

(7, 4),

(9, 3.8),

(11, 4),

(13, 3),

(15, 1),

(17, 0.5),

(19, 0),

]

ampl.param["unit_cost"] = 2 # Unit cost of the product

ampl.param["n_step"] = len(data) # Number of discrete steps in the data

demand_param = ampl.getParameter("demand") # Get the 'demand' parameter

price_param = ampl.getParameter("price") # Get the 'price' parameter

for i, (demand_value, price_value) in enumerate(

data, start=1

): # Loop through data points

demand_param.set(i, demand_value) # Assign demand value to each step

price_param.set(i, price_value) # Assign price value to each step

3.3. Solve problem#

# Set the solver type for use in solving the problems

solver = "cplex" # Use CBC solver for optimization tasks

ampl.option["show_stats"] = 0 # Show problem size statistics (default: 0)

ampl.option["display_1col"] = 0 # Disable single-column data display

# ampl.option['omit_zero_rows'] = 1 # Hide rows with zero values

# ampl.option['omit_zero_cols'] = 1 # Hide columns with zero values

ampl.option["mp_options"] = (

"outlev=1 lim:time=20" # Configure CBC options (output level and time limit)

)

ampl.solve(

solver=solver, verbose=False

) # Solve the optimization problem using CBC solver

assert ampl.solve_result == "solved", ampl.solve_result

3.4. Display results#

# Display results for key variables

ampl.display("_varname", "_var", "_var.lb", "_var.ub", "_var.rc", "_var.slack")

ampl.display("_conname", "_con", "_con.body", "_con.lb", "_con.ub", "_con.slack")

ampl.display("_objname", "_obj")

: _varname _var _var.lb _var.ub _var.rc _var.slack :=

1 'IsSelect[1]' 0 0 1 8 0

2 'IsSelect[2]' 0 0 1 15 0

3 'IsSelect[3]' 0 0 1 15 0

4 'IsSelect[4]' 0 0 1 14 0

5 'IsSelect[5]' 0 0 1 16.2 0

6 'IsSelect[6]' 1 0 1 22 0

7 'IsSelect[7]' 0 0 1 13 0

8 'IsSelect[8]' 0 0 1 -15 0

9 'IsSelect[9]' 0 0 1 -25.5 0

10 'IsSelect[10]' 0 0 1 -38 0

;

: _conname _con _con.body _con.lb _con.ub _con.slack :=

1 OnePriceSelected 0 1 1 1 0

;

: _objname _obj :=

1 TotalProfit 22

;

4. Approach#2 (Maximum demand for optimal price)#

Ultimately, this approach determines the maximum demand for a given price level by the key points.

4.1. AMPL Model Formulation#

%%writefile demand_elasticity_1_model.mod

reset;

# Model Name: # Pricing Optimization

# Description: This model maximizes total revenue by selecting the optimal price step and managing quantity sold under piecewise linear pricing.

# Version: 1.0

# Last Updated: Jan 2025

### PARAMETERS

# Input parameters defining total quantity, cost, price steps, and demand

param unit_cost >= 0; # Unit cost of the product

param n_step integer > 0; # Number of steps in the piecewise linear price function

param demand {1..n_step+1} >= 0; # Demand values at each price step

param price {1..n_step+1} >= 0; # Price values for each demand step

### VARIABLES

# Decision variables for managing quantity and selecting price steps

var IsSelect {1..n_step} binary; # Binary decision variable: 1 if point is selected, 0 otherwise

var Quantity_Sold {1..n_step} >= 0, integer; # Quantity sold at each price step

### OBJECTIVE

maximize Total_Profit: # Maximize total revenue from sales while considering costs and constraints

sum{i in 1..n_step} Quantity_Sold[i] * (price[i] - unit_cost);

### CONSTRAINTS

# Ensure logical and physical constraints are met

s.t. OnePriceSelected: # Only one price step can be selected

sum {i in 1..n_step} IsSelect[i] = 1;

s.t. Demand_Upper_Bound {i in 1..n_step-1}:# Quantity sold must align with selected price step

Quantity_Sold[i] <= (demand[i+1] - 0.0001) * IsSelect[i] ;

Overwriting demand_elasticity_1_model.mod

4.2. Load data#

ampl.read("demand_elasticity_1_model.mod") # Load the AMPL model from the file

# Data for demand and price

data = [

(1, 10),

(3, 7),

(5, 5),

(7, 4),

(9, 3.8),

(11, 4),

(13, 3),

(15, 1),

(17, 0.5),

(19, 0),

]

ampl.param["unit_cost"] = 2 # Unit cost of the product

ampl.param["n_step"] = len(data) - 1 # Number of discrete steps in the data

demand_param = ampl.getParameter("demand") # Get the 'demand' parameter

price_param = ampl.getParameter("price") # Get the 'price' parameter

for i, (demand_value, price_value) in enumerate(

data, start=1

): # Loop through data points

demand_param.set(i, demand_value) # Assign demand value to each step

price_param.set(i, price_value) # Assign price value to each step

4.3. Solve problem#

# Set the solver type for use in solving the problems

solver = "cplex" # Use CBC solver for optimization tasks

ampl.option["show_stats"] = 0 # Show problem size statistics (default: 0)

ampl.option["display_1col"] = 0 # Disable single-column data display

# ampl.option['omit_zero_rows'] = 1 # Hide rows with zero values

# ampl.option['omit_zero_cols'] = 1 # Hide columns with zero values

ampl.option["mp_options"] = (

"outlev=1 lim:time=20" # Configure CBC options (output level and time limit)

)

ampl.solve(

solver=solver, verbose=False

) # Solve the optimization problem using CBC solver

assert ampl.solve_result == "solved", ampl.solve_result

4.4. Display results#

# Display results for key variables

ampl.display("_varname", "_var", "_var.lb", "_var.ub", "_var.rc", "_var.slack")

ampl.display("_conname", "_con", "_con.body", "_con.lb", "_con.ub", "_con.slack")

ampl.display("_objname", "_obj")

: _varname _var _var.lb _var.ub _var.rc _var.slack :=

1 'IsSelect[1]' 0 0 1 0 0

2 'IsSelect[2]' 0 0 1 0 0

3 'IsSelect[3]' 0 0 1 0 0

4 'IsSelect[4]' 0 0 1 0 0

5 'IsSelect[5]' 0 0 1 0 0

6 'IsSelect[6]' 1 0 1 0 0

7 'IsSelect[7]' 0 0 1 0 0

8 'IsSelect[8]' 0 0 1 0 0

9 'IsSelect[9]' 0 0 1 0 0

10 'Quantity_Sold[1]' 0 0 2 8 0

11 'Quantity_Sold[2]' 0 0 4 5 0

12 'Quantity_Sold[3]' 0 0 6 3 0

13 'Quantity_Sold[4]' 0 0 8 2 0

14 'Quantity_Sold[5]' 0 0 10 1.8 0

15 'Quantity_Sold[6]' 12 0 12 2 0

16 'Quantity_Sold[7]' 0 0 14 1 0

17 'Quantity_Sold[8]' 0 0 16 -1 0

18 'Quantity_Sold[9]' 0 0 Infinity -1.5 0

;

: _conname _con _con.body _con.lb _con.ub _con.slack :=

1 OnePriceSelected 0 1 1 1 0

2 'Demand_Upper_Bound[1]' 0 0 -Infinity 0 0

3 'Demand_Upper_Bound[2]' 0 0 -Infinity 0 0

4 'Demand_Upper_Bound[3]' 0 0 -Infinity 0 0

5 'Demand_Upper_Bound[4]' 0 0 -Infinity 0 0

6 'Demand_Upper_Bound[5]' 0 0 -Infinity 0 0

7 'Demand_Upper_Bound[6]' 0 -0.9999 -Infinity 0 0.9999

8 'Demand_Upper_Bound[7]' 0 0 -Infinity 0 0

9 'Demand_Upper_Bound[8]' 0 0 -Infinity 0 0

;

: _objname _obj :=

1 Total_Profit 24

;

5. Approach#3 (Using the built-in AMPL piecewise linear function)#

5.1. AMPL Model Formulation#

%%writefile demand_elasticity_2_model.mod

reset;

# Model Name: Pricing Optimization (AMPL Piecewise construction for Price Elasticity of Demand)

# Version: 1.0

# Last Updated: Jan 2025

### PARAMETERS

# Input parameters defining total quantity, cost, price steps, and demand

param unit_cost >= 0; # Unit cost of the product

param n_step integer > 0; # Number of steps in the piecewise linear price function

param demand {1..n_step+1} >= 0; # Demand values at each price step

param price {1..n_step+1} >= 0; # Price values for each demand step

### VARIABLES

# Decision variables for managing quantity and selecting price steps

var IsSelect {1..n_step} binary; # Binary decision variable: 1 if point is selected, 0 otherwise

var Quantity_Sold {1..n_step} >= 0, integer; # Quantity sold at each price step

### OBJECTIVE

maximize Total_Profit: # Maximize total revenue from sales while considering costs and constraints

sum {i in 1..n_step}

<<demand[i]; {p in i..i+1} (price[p]- unit_cost)>> Quantity_Sold[i];

# Find more information about the piecewise linear function: https://ampl.com/wp-content/uploads/Chapter-17-Piecewise-Linear-Programs-AMPL-Book.pdf

### CONSTRAINTS

# Ensure logical and physical constraints are met

s.t. OnePriceSelected: # Only one price step can be selected

sum {i in 1..n_step} IsSelect[i] = 1;

s.t. Demand_Upper_Bound {i in 1..n_step-1}:# Quantity sold must align with selected price step

Quantity_Sold[i] <= (demand[i+1] - 0.0001) * IsSelect[i] ;

Overwriting demand_elasticity_2_model.mod

5.2. Load data#

ampl.read("demand_elasticity_2_model.mod") # Load the AMPL model from the file

# Data for demand and price

data = [

(1, 10),

(3, 7),

(5, 5),

(7, 4),

(9, 3.8),

(11, 4),

(13, 3),

(15, 1),

(17, 0.5),

(19, 0),

]

ampl.param["unit_cost"] = 2 # Unit cost of the product

ampl.param["n_step"] = len(data) - 1 # Number of discrete steps in the data

demand_param = ampl.getParameter("demand") # Get the 'demand' parameter

price_param = ampl.getParameter("price") # Get the 'price' parameter

for i, (demand_value, price_value) in enumerate(

data, start=1

): # Loop through data points

demand_param.set(i, demand_value) # Assign demand value to each step

price_param.set(i, price_value) # Assign price value to each step

5.3. Solve problem#

# Set the solver type for use in solving the problems

solver = "cplex" # Use CBC solver for optimization tasks

ampl.option["show_stats"] = 0 # Show problem size statistics (default: 0)

ampl.option["display_1col"] = 0 # Disable single-column data display

# ampl.option['omit_zero_rows'] = 1 # Hide rows with zero values

# ampl.option['omit_zero_cols'] = 1 # Hide columns with zero values

ampl.option["mp_options"] = (

"outlev=1 lim:time=20" # Configure CBC options (output level and time limit)

)

ampl.solve(

solver=solver, verbose=False

) # Solve the optimization problem using CBC solver

assert ampl.solve_result == "solved", ampl.solve_result

5.4. Display results#

# Display results for key variables

ampl.display("_varname", "_var", "_var.lb", "_var.ub", "_var.rc", "_var.slack")

ampl.display("_conname", "_con", "_con.body", "_con.lb", "_con.ub", "_con.slack")

ampl.display("_objname", "_obj")

: _varname _var _var.lb _var.ub _var.rc _var.slack :=

1 'IsSelect[1]' 0 0 1 0 0

2 'IsSelect[2]' 0 0 1 0 0

3 'IsSelect[3]' 0 0 1 0 0

4 'IsSelect[4]' 0 0 1 0 0

5 'IsSelect[5]' 0 0 1 0 0

6 'IsSelect[6]' 1 0 1 0 0

7 'IsSelect[7]' 0 0 1 0 0

8 'IsSelect[8]' 0 0 1 0 0

9 'IsSelect[9]' 0 0 1 0 0

10 'Quantity_Sold[1]' 0 0 2 8 0

11 'Quantity_Sold[2]' 0 0 4 5 0

12 'Quantity_Sold[3]' 0 0 6 3 0

13 'Quantity_Sold[4]' 0 0 8 2 0

14 'Quantity_Sold[5]' 0 0 10 1.8 0

15 'Quantity_Sold[6]' 12 0 12 0 0

16 'Quantity_Sold[7]' 0 0 14 1 0

17 'Quantity_Sold[8]' 0 0 16 0 0

18 'Quantity_Sold[9]' 0 0 Infinity 0 0

;

: _conname _con _con.body _con.lb _con.ub _con.slack :=

1 OnePriceSelected 0 1 1 1 0

2 'Demand_Upper_Bound[1]' 0 0 -Infinity 0 0

3 'Demand_Upper_Bound[2]' 0 0 -Infinity 0 0

4 'Demand_Upper_Bound[3]' 0 0 -Infinity 0 0

5 'Demand_Upper_Bound[4]' 0 0 -Infinity 0 0

6 'Demand_Upper_Bound[5]' 0 0 -Infinity 0 0

7 'Demand_Upper_Bound[6]' 0 -0.9999 -Infinity 0 0.9999

8 'Demand_Upper_Bound[7]' 0 0 -Infinity 0 0

9 'Demand_Upper_Bound[8]' 0 0 -Infinity 0 0

;

: _objname _obj :=

1 Total_Profit 23

;

6. Function Refinement (linear interpolation of data between nodes)#

6.1. Linear interpolation#

from scipy.interpolate import interp1d

ampl.read("demand_elasticity_2_model.mod") # Load the AMPL model from the file

# Define the data points as (X, Y) pairs

data = [

(1, 10),

(3, 7),

(5, 5),

(7, 4),

(9, 3.8),

(11, 4),

(13, 3),

(15, 1),

(17, 0.5),

(19, 0),

]

x_points, y_points = zip(*data) # Extract X and Y values from the data points

x_points = [x * 1 for x in x_points] # Multiply each x_point by 1

y_points = [y * 1 for y in y_points] # Multiply each y_point by 1

linear_interp = interp1d(

x_points, y_points, kind="linear"

) # Create the linear interpolator

# Generate new points and compute X*Y

x_new = np.arange(min(x_points), max(x_points) + 1) # Integer X values

y_new = linear_interp(x_new) # Interpolated Y values

interpolated_points = [

(int(x), float(y)) for x, y in zip(x_new, y_new)

] # Combine the new points and X*Y values

# Set data for AMPL

ampl.param["unit_cost"] = 2 # Unit cost of the product

# !!!! (-1 for demand_elasticity_2_model.mod)

ampl.param["n_step"] = (

len(interpolated_points) - 1

) # Number of discrete steps in the data

ampl.param["demand"] = {i + 1: p[0] for i, p in enumerate(interpolated_points)}

ampl.param["price"] = {i + 1: p[1] for i, p in enumerate(interpolated_points)}

6.2. Solve problem & Display results#

# Set the solver type for use in solving the problems

solver = "cbc" # Use CBC solver for optimization tasks

ampl.option["show_stats"] = 1 # Show problem size statistics (default: 0)

ampl.option["display_1col"] = 0 # Disable single-column data display

ampl.option["_solve_time"] = 1

# ampl.option['omit_zero_rows'] = 1 # Hide rows with zero values

# ampl.option['omit_zero_cols'] = 1 # Hide columns with zero values

ampl.option["mp_options"] = (

"outlev=1 lim:time=20" # Configure CBC options (output level and time limit)

)

ampl.solve(

solver=solver, verbose=False

) # Solve the optimization problem using CBC solver

assert ampl.solve_result == "solved", ampl.solve_result

# Display results for key variables

ampl.display("_varname", "_var", "_var.lb", "_var.ub", "_var.rc", "_var.slack")

ampl.display("_conname", "_con", "_con.body", "_con.lb", "_con.ub", "_con.slack")

ampl.display("_objname", "_obj")

: _varname _var _var.lb _var.ub _var.rc _var.slack :=

1 'IsSelect[1]' 0 0 1 0 0

2 'IsSelect[2]' 0 0 1 0 0

3 'IsSelect[3]' 0 0 1 0 0

4 'IsSelect[4]' 0 0 1 0 0

5 'IsSelect[5]' 0 0 1 0 0

6 'IsSelect[6]' 0 0 1 0 0

7 'IsSelect[7]' 0 0 1 0 0

8 'IsSelect[8]' 0 0 1 0 0

9 'IsSelect[9]' 0 0 1 0 0

10 'IsSelect[10]' 0 0 1 0 0

11 'IsSelect[11]' 1 0 1 0 0

12 'IsSelect[12]' 0 0 1 0 0

13 'IsSelect[13]' 0 0 1 0 0

14 'IsSelect[14]' 0 0 1 0 0

15 'IsSelect[15]' 0 0 1 0 0

16 'IsSelect[16]' 0 0 1 0 0

17 'IsSelect[17]' 0 0 1 0 0

18 'IsSelect[18]' 0 0 1 0 0

19 'Quantity_Sold[1]' 0 0 1 0 0

20 'Quantity_Sold[2]' 0 0 2 0 0

21 'Quantity_Sold[3]' 0 0 3 0 0

22 'Quantity_Sold[4]' 0 0 4 0 0

23 'Quantity_Sold[5]' 0 0 5 0 0

24 'Quantity_Sold[6]' 0 0 6 0 0

25 'Quantity_Sold[7]' 0 0 7 0 0

26 'Quantity_Sold[8]' 0 0 8 0 0

27 'Quantity_Sold[9]' 0 0 9 0 0

28 'Quantity_Sold[10]' 0 0 10 0 0

29 'Quantity_Sold[11]' 11 0 11 0 0

30 'Quantity_Sold[12]' 0 0 12 0 0

31 'Quantity_Sold[13]' 0 0 13 0 0

32 'Quantity_Sold[14]' 0 0 14 0 0

33 'Quantity_Sold[15]' 0 0 15 0 0

34 'Quantity_Sold[16]' 0 0 16 0 0

35 'Quantity_Sold[17]' 0 0 17 0 0

36 'Quantity_Sold[18]' 0 0 Infinity 0 0

;

: _conname _con _con.body _con.lb _con.ub _con.slack

:=

1 OnePriceSelected 0 1 1 1 0

2 'Demand_Upper_Bound[1]' 0 0 -Infinity 0 0

3 'Demand_Upper_Bound[2]' 0 0 -Infinity 0 0

4 'Demand_Upper_Bound[3]' 0 0 -Infinity 0 0

5 'Demand_Upper_Bound[4]' 0 0 -Infinity 0 0

6 'Demand_Upper_Bound[5]' 0 0 -Infinity 0 0

7 'Demand_Upper_Bound[6]' 0 0 -Infinity 0 0

8 'Demand_Upper_Bound[7]' 0 0 -Infinity 0 0

9 'Demand_Upper_Bound[8]' 0 0 -Infinity 0 0

10 'Demand_Upper_Bound[9]' 0 0 -Infinity 0 0

11 'Demand_Upper_Bound[10]' 0 0 -Infinity 0 0

12 'Demand_Upper_Bound[11]' 0 -0.9999 -Infinity 0 0.9999

13 'Demand_Upper_Bound[12]' 0 0 -Infinity 0 0

14 'Demand_Upper_Bound[13]' 0 0 -Infinity 0 0

15 'Demand_Upper_Bound[14]' 0 0 -Infinity 0 0

16 'Demand_Upper_Bound[15]' 0 0 -Infinity 0 0

17 'Demand_Upper_Bound[16]' 0 0 -Infinity 0 0

18 'Demand_Upper_Bound[17]' 0 0 -Infinity 0 0

;

: _objname _obj :=

1 Total_Profit 22

;

7. Retrieve solution in Python#

# Initialize an empty dictionary to store AMPL variable data

amplvar = dict()

# Prepare a list of AMPL variables

list_of_ampl_variables = [item[0] for item in ampl.get_variables()]

# Iterate over each variable name in the list

for key_ampl in list_of_ampl_variables:

# Skip certain variables that are not to be processed (these variables won't be included in the output)

if key_ampl not in [""]:

# Convert the AMPL variable data to a pandas DataFrame

df = ampl.var[key_ampl].to_pandas()

# Filter the DataFrame to include only rows where the variable's value is greater than a small threshold (1e-5)

filtered_df = df[df[f"{key_ampl}.val"] > 1e-5]

# Round the values in the DataFrame to two decimal places

rounded_df = filtered_df.round(2)

# Convert the filtered DataFrame to a dictionary and add it to the amplvar dictionary

amplvar[key_ampl] = rounded_df # .to_dict(orient='records')

print(amplvar[key_ampl])

Quantity_Sold.val

11 11

8. Comparison of performance of different approaches#

Performance measurements were performed over the period

x_points = [x * 100 for x in x_points] # Multiply each x_point by 100

y_points = [y * 100 for y in y_points] # Multiply each y_point by 100

| Approach#1 | |||||||||||||

| Approach#2 | |||||||||||||

| Approach#3 | |||||||||||||

9. Visualization of the data and solution#

import matplotlib.pyplot as plt

# Separate the data into X and Y values

x_values, y_values = zip(*interpolated_points)

# Find the y-coordinate

x_target = amplvar["Quantity_Sold"]["Quantity_Sold.val"].iloc[0]

if x_target in x_values:

y_target = y_values[x_values.index(x_target)]

else:

# Interpolate y-coordinate if x_target is not in x_values

from scipy.interpolate import interp1d

interpolation_function = interp1d(x_values, y_values, kind="linear")

y_target = interpolation_function(x_target)

# Create a plot

plt.figure(figsize=(10, 6)) # Set the figure size

plt.plot(

x_values, y_values, marker="o", linestyle="-", color="b", label="Demand Elasticity"

)

# Add a vertical line at x = 1100

plt.axvline(x=x_target, color="r", linestyle="--", label=f"x = {x_target}")

# Add a horizontal line at the intersection point

plt.axhline(y=y_target, color="g", linestyle="--", label=f"y = {y_target:.2f}")

# Mark the intersection point

plt.scatter(

[x_target], [y_target], color="purple", zorder=5, label="Intersection Point"

)

# Customize the plot

plt.title("Demand Elasticity", fontsize=16)

plt.xlabel("Demand", fontsize=12)

plt.ylabel("Price", fontsize=12)

plt.grid(True, linestyle="--", alpha=0.7) # Add a grid

plt.legend(fontsize=12) # Add a legend

# Show the plot

plt.show()

print("Keys in amplvar:", amplvar.keys())

Keys in amplvar: dict_keys(['IsSelect', 'Quantity_Sold'])